I’m hoping my gentle accounting-dweeby readers can help me.

I’m very interested in looking at economic measures (i.e. debt/lending/borrowing) for the U.S. “real” sector: households plus nonfinancial business.

My problem: with some exceptions, various national accounts (NIPA, FOFA, IMA) don’t provide tables for this “sector.”

I don’t think I can simply sum up household and nonfinancial business, because some of the lending/borrowing is between these two sectors. Is it possible to net that out based on published tables?

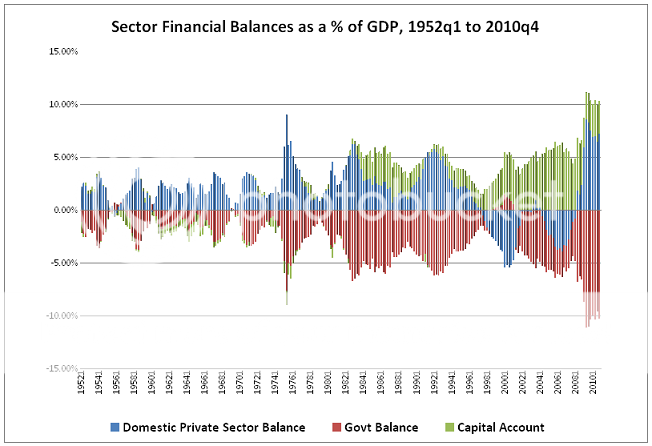

I’d really like to see a sectoral balance chart (really a “balance of flows”) displaying the following sectors:

{kind=link}

Domestic Real

Domestic Financial

Government

Rest of World

I’d really love to see the lending/borrowing flows from each sector, to each other sector. Sized arrows between each. Is this possible?

That sectoral breakout is tricky, of course, because firms — especially financial firms — are heavily engaged in ROW. Is it even possible to realistically estimate the financial sector as a purely domestic entity?

Any thoughts and suggestions are welcome. Thanks.

Update: A further condundrum: at least in the FOFAs, hedge funds are tallied under Households. This is presumably because like households but unlike commercial banks, they’re not licensed/chartered to print new money for lending (at least nominally, technically…). To the extent that “hedge funds” includes the whole goddam shadow-banking industry (?), it seems like this would (wildly?) distort numbers for the household hence the real sector. Also: Several banks and holding companies, i.e. Goldman Sachs, magically transformed themselves into commercial banks during the financial crisis, so they could tap bailout funds. How did national accountants deal with that? How would it affect time series of debt/lending/borrowing for the financial and real sectors?

Comments

8 responses to “Bleg: Accounting for the Real Sector”

Not sure what are asking.

Doesn’t the Fed Z.1 http://www.federalreserve.gov/releases/z1/Current/z1.pdf Table F.8 and Table S.2.a include what you are looking for?

@Ramanan

Are you saying:

Summing HH net L/B and nonfin biz net L/B will yield the same number, no matter what the lending and borrowing is between HHs and nonfin biz.

??

Tabling it out, that seems to be true.

But I’d still like to see the flows broken out:

i.e.: What’s net lending/borrowing between HHs and Financial biz? Between HHs and Fin biz?

Any way to pull that?

@Asymptosis

The concept “net lending” is really a concept which makes sense after having summed up everything.

I don’t think “net lending of households to the financial sector” has any meaning. There should be a different phrase/terminology for that.

I’m wondering what your intuitive reason is for this question.

You can construct a single balance sheet for the domestic financial sector, which will obvious be enormous in size into the tens of $ trillions. It will be in balance like all balance sheets. Likewise you can construct a flow of funds statement.

So you’re going to see massive flows in and out.

That will include all household holdings of deposits and the value of financial assets that are the liabilities of insurance companies, pension funds, mutual funds, etc.

From a household perspective, what won’t will be included is residential real estate and financial claims held directly on non-financial firms such as directly held stocks and bonds.

And similarly for the corporate interaction with the financial sector balance sheet, and for the other side of that balance sheet, etc. etc.

But what are you after in this?

Why do you want to exclude the financial sector when it is so massively central to the balance sheet structure of the entire economy?

Are you after some sort of counterfactual arrangement?

What would it be? Banks and insurance companies and mutual funds do act as financial intermediaries with specific roles in this context.

@Ramanan “I don’t think “net lending of households to the financial sector†has any meaning. There should be a different phrase/terminology for that.”

That is a very interesting statement. Same for nonfin business? Why doesn’t it make sense?

Interesting because the central conceit is that the financial sector intermediates by borrowing short (from HHs) and lending long (to firms). Yes, simplified, but that’s the model that people (very much including economists) carry around in their heads. If what you say is true, what does it mean for that concept?

What word(s) would you uses to describe that net flow?

@JKH:

I’m interested in the sector that does (almost all of) the producing and consuming. Over the decades, how has its relationship to the financial sector changed? Are there big secular changes that give insight into things that interest me, like inequality and economic growth?

I’d like to look at the flow-balance graph, for instance, while reading this Josh Mason paper:

http://repec.umb.edu/RePEc/files/FisherDynamics.pdf

And thinking: what would this paper say if it was talking about the whole real sector?

I’m realizing a two-sector graph — real and everything else — might give useful insights on how things have changed over the decades.

You make a good point: do pension fund assets (etc.) get imputed to household balance sheets? Hmmm…. This may go straight to Ramanan’s statement above.

One of my main ways of learning and figuring things out is looking at numbers lots of different ways. My intuition is just that this way might teach me something about historical economic dynamics, though I’m not sure what until I see it.

@Asymptosis

“Why doesn’t it make sense?”

I think it is because the type of balance you are thinking is more about the current account than financial account. So I can what’s the trade balance of India with China in addition to overall trade balance similarly one can ask the income one sector receives from a sector to outlays to that sector. But the financial account counterpart makes less sense.

Hope this is still of interest to you.

I’ve been curious about the possibility of reconciling the flow-of-funds (FFA) and NIPA accounts also , and apparently there’s been a big push to do that , in both the national and international context. I gather the IMA will be the designated meeting point , if they ever get it all nailed down.

Anyway , you might like to take a look at this paper , which has some nice illustrations comparing data from the capital/current accounts of NIPA with those of the FOF financial accounts :

http://www.nber.org/chapters/c12834.pdf

There’s also been an attempt to update the more granular HH data from the SCF in-between the triennial surveys , by “ageing” the previous data with help from FFA info :

http://www.stlouisfed.org/household-financial-stability/events/20130205/papers/Sabelhaus_Moore_Smith.pdf