Reading the many web comments on my flat tax proposal, I find that many didn’t actually read it (I do go on…), or understand it.

So here’s the short version. Not so short, as it turns out, but I hope easier to grasp quickly.

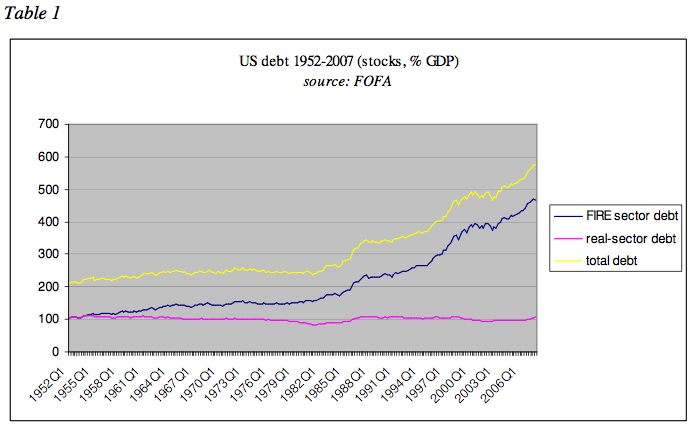

Unlike the many commenters who failed to do so, please at least skim through before commenting, here or elsewhere. For supporting data and graphics, and sources, see the original post.

The proposal:

1. Tax financial assets of domestic entities, personal and corporate, at an annual rate of 1%, generating revenues somewhere north of $550 billion a year.

2. Eradicate corporate, dividend, and capital-gains taxes, and reduce income taxes by 22–51%.

The implications, and responses to objections:

• Because there would be no taxes on real, productive assets (structures, equipment, software, and the less-measurable assets derived from training, R&D, organization building, etc.) or profits, and personal income would be taxed at a much lower rate, the Financial Assets Tax (FAT tax) would encourage investment spending on real assets (and consumption) instead of hoarding of money in financial assets — living off the economically useless (at least in the long term) “rents” from those holdings.

• In other words, the FAT would discourage saving (storing money in financial assets) in favor of investment spending (and consumption).

• We currently tax worldwide income (at least of natural humans). There’s no reason we can’t tax worldwide holdings; it’s actually much easier. It would end the tax-avoidance scheme of corporations indefinitely “deferring” taxes on un-repatriated offshore income.

• People and companies will still seek to engage in tax fraud by concealing their international holdings, just as they now attempt to conceal their international incomes. Nothing new there, except that income flows are easier to hide than holdings.

• Since financial holdings would be taxed no matter where they are stored, Americans would have incentive (convenience, security, etc.) to store them domestically. (Worth actually reading for those who haven’t: Adam Smith’s “invisible hand” passage.)

• Since corporate profits would not be taxed, multinational corporations would have incentive to repatriate their worldwide profits — something that is actively discouraged by the current tax regime. Constraints on inbound money flows (“foreign” direct investment) would thus be reduced.

• It doesn’t much matter to our country where financial assets reside. It very much matters where real assets reside — they are what constitute our national wealth: our means of producing (and consuming) in the future.

• If there are attractive and lucrative real-investment opportunities in America, money (so-called financial “capital”) will flow into those investments. It doesn’t matter where the money is currently stored.

• Even acknowledging some “friction” in international money flows (though it’s darned hard to discern that friction), businesses consistently tell us that shortage of financing is the very last thing on their list of business constraints. Fact: The supply of credit to the real economy far exceeds the demand. The supply of liquidity is truly oceanic, and over recent decades that supply has expanded at a far faster pace than the demand, with all of the excess going to the financial sector.

{kind=link}

• Havens for financial assets like the Bahamas and Lichtenstein, despite their massive holdings of financial assets, do not become economic powerhouses. This is because simply harboring financial assets does not result in formation of real assets.

• The American financial sector would shrink as people moved money to real assets. This would shift some income from real, productive activities in the financial sector (advice, intermediation, bookkeeping, etc.) to other, arguably more productive, activities in the real sector.

• Credit-issuance to the financial sector would decline because financial-sector returns would decline, reducing the systemic “meltdown” risks associated with excessive quantities of debt, especially financial-sector debt.

• Fluctuations in a smaller financial assets market — the sole or at least primary source of so-called “business cycles” — would result in smaller disruptions to the real economy.

• A smaller financial sector, and and an annual tax on private wealth, would over time reduce the concentrations of wealth that result in government capture.

• A smaller financial sector would have less blackmail leverage to demand bailouts when it screws up. Moral hazard and all that.

• Lower returns on financial assets would decrease the incentives for brilliant people to earn their livings from “rent-seeking” in the financial sector, better allocating those human resources to productive, real-sector activities.

• Reducing or eliminating taxes on income and profits would remove or reduce major economic distortions/mis-incentives — discouraging work and entrepreneurship.

• Taxing financial wealth would introduce very little economic distortion, because there is no substitute for wealth, so the demand for wealth is largely inelastic. (Unlike the demand for employment, which is quite elastic because there is an excellent substitute: leisure.)

• Taxing financial assets would to some extent correct for a distortion inherent to the artificial nature of the financial system: real assets decay while financial assets do not, so real assets are at a great disadvantage when competing for “investment.”

• A financial assets tax would be very progressive, because the distribution of financial assets is very regressive. This would help make the overall tax structure (fed, state, local combined) actually progressive, which it currently is not above about $60K or $80K in annual income.

{kind=link}

• The wider distribution of wealth and income resulting from a Financial Assets Tax would better harness the “wisdom of the crowds,” cycling more money through consumption purchases to producers who deliver things that people actually want. (Rather than relying on omniscient asset allocation by a small cadre of suppliers and arbitragers.)

• The overall U.S. tax regime would be much more equitable — fairer.

I should add one last thing: we could achieve much the same effect through slightly (1%) higher inflation — making financial assets less valuable and real assets more valuable. But being something of a constitutional conservative like Obama, I think that ideally such a move should be effected by legislative intent, rather than the machinations of unelected technocrats at the Fed. Also — I won’t go through all the technical mechanics here — I think the taxing approach would result in less economic distortion.

Comments

6 responses to “The Flat Tax, Short Version”

I still don’t know why somebody who makes $35,000 a year in wages/salary should pay an income tax, but somebody who makes $35,000 a year in dividends, or capital gains, whichever, should not. Pick any number higher than that, or lower than that, I’d still object that those who benefit entirely from capital ought to carry their share…(but I don’t believe that those who live off capital should be exempted from FICA/SS either….) After all, they do what they do for themselves, not for me.

@Dave Raithel, I couldn’t agree more — even though I is one of those rentiers.

In your example, assume the financial investor is earning 6%. That means he’s got about $583,000. He’d be taxed $5833, or about 17% of income. (I didn’t even get into the possibility of a progressive tax on financial assets…)

I also tend to agree with you about payroll taxes, but that’s at heart a political issue conjoined to a funding issue. See here:

http://www.asymptosis.com/is-the-social-security-trust-fund-a-liberal-own-goal.html

Too bad about that, because by removing the income cap on SS we would generate *exactly* the amount necessary — 0.6% of GDP — to make SS solvent beyond the foreseeable future.

Medicare and Medicaid are a whole ‘nother issue, of course.

[…] Asymptosis – “The Flat Tax, Short Version” […]

Sorry, I’m very late getting here.

I did read the original post, and this one.

You thinking is original and clear, and has some appeal. But there are abstractions that might or might not play out in the real world.

The financial sector is so big and powerful, that it is hard for me to believe in the automatic shrinkage you anticipate.

Reducing or eliminating taxes on income and profits would remove or reduce major economic distortions/mis-incentives — discouraging work and entrepreneurship.

IMHO, this “misincentive” is either wildly overstated or non-existent. Further, as a result of direct or amortization accounting expense, investment reduces current taxes, and thus taxation provides an incentive, and higher tax rates even more so. Perhaps this is a distortion, but I really don’t think so.

Since financial holdings would be taxed no matter where they are stored, Americans would have incentive (convenience, security, etc.) to store them domestically.

I think you are overstating the incentive. What happens is you are removing a disincentive. Couldn’t the result be incentive-neutral? Ditto the following point on corp profits. While removing the disincentives will enable some opportunities, they will not actively encourage them, so the net effect would be far less than you are suggesting.

I do like your outside-the-cashbox thinking.

Cheers!

JzB

[…] inflation would be quite similar in its effects to the financial assets tax that I proposed a while back, and carry the benefits I describe […]

I finally found someone besides myself who has half a brain and realizes that America is worth $131 trillion and therefore $3.54T is only 2.7% of that.

I’d love to tell people that we should just tax that 131 trillion at 2.7% and get rid of all taxes entirely, but it’s SO HARD to get fuckin libertarians, conservatives, and even liberals to know wtf you’re talking about.

My version of this (have had many, but most recent version) is to “tax” that 131T through giving the IRS control over the international exchange rate of the dollar. I googled the “m1 or m0” data for the US and found that the cash part of America’s financial assets seems to be only 2.7T or so. After googling things like ‘market capitalization’ and ‘world capital markets’ I found that indeed, like 99% of America’s financial assets seem to be like non-cash (basically stocks).

My only concern with a financial asset tax (FAT) is that they’d find some kind of bullshit loophole to store financial assets in another country or something. So, that’s why I thought it’d be much easier to just give the IRS control over the global international exchange rate of the dollar. I figured you just multiply that number by .97, wire yourself 3.5T, and call it a day.

It’s SO HARD though to get fucking assholes on the internet to understand anything. Most people have no clue what fractional reserve lending even is, and have been brainwashed into believing that all banks and governments do is inflate currency and that’s it. The basic engine of economic expansion is unknown to them, but no: they think they know everything. SO many fucking smug brainwashed sons of bitches. hooooly shit 🙁