Comes to mind: the one about the two British ladies who meet at the Ascot races.

“My dear,” says the first. “What a lovely hat. Where did you get it?”

“Oh darling,” says the second, looking somewhat pained, “don’t you know, we have our hats.”

It comes to mind as I ponder the rather grudging and tepid suggestions that you hear here and there these days — that excessive inequality might actually be a drag on economic growth and prosperity. There are some full-throated assertions of this belief out there, but in the mainstream economics community they are rare and in general quite decidedly mealy-mouthed. (No names, just initials: The Economist.)

The general failure to question the “more inequality is good for growth” mantra has deep roots, even among progressive economists. Viz, this from Paul Krugman back in December, 2008, when the highest inequality since The Great Depression was was in the process of delivering the first (at least potential) depression since…The Great Depression (bold mine):

There’s no obvious reason why consumer demand can’t be sustained by the spending of the upper class — $200 dinners and luxury hotels create jobs, the same way that fast food dinners and Motel 6s do. In fact, the prosperity of New York City in the last decade — largely supported off of super-salaried Wall Street types — is a demonstration that you can have an economy sustained by the big spending of the few rather than the modest spending of large numbers of people.

This seems to completely ignore marginal propensity to consume (MPC) — that poorer people spend a larger percentage of their income than rich people, so a more equal income distribution would result in higher money velocity, hence higher GDP. (I have seen no indication that Krugman’s opinion on this subject has changed since then.)

But I’d like to suggest that the problem runs deeper. Almost all the thinking about MPC seems to obsess about income, and greatly downplay the role of wealth, or net worth. The Wikipedia article on MPC, for instance, includes only one passing mention of wealth.

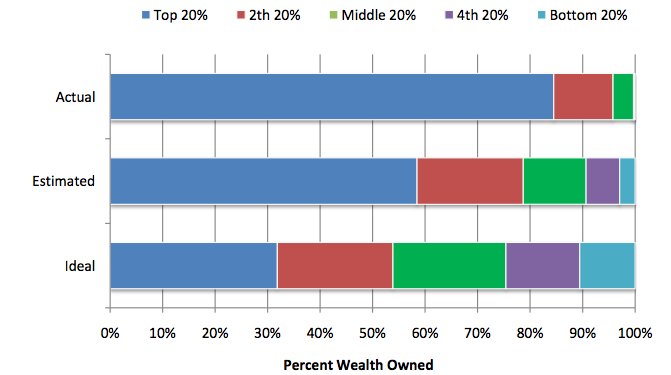

This failure to consider wealth is important because wealth inequality in this country (and worldwide) utterly dwarfs income inequality.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The Friedman/Modigliani rational-expectations lifecycle-hypothesis school does include wealth in their theories of marginal propensity to consume, but they assume that a great deal of people’s “wealth” actually consists of expected future income. This in turn assumes consumers’ excellent foresight decades into the future, and that people (at all income levels) are able or even likely to engage (accurately) in net-present-value calculations of their future incomes and expenditures.

There’s obviously a large literature on this subject that is ridiculously condensed above. But that aside: for thinking purposes I’d like to propose an admittedly simplified, opposite model that I have not seen discussed, in which current wealth (individual net worth) is the only determinant of (consumption) spending in a given period.

Imagine a world with eleven people in it, where we all have our wealth, and where net worth is broken out as follows.

Person 1: $1,000,000

Persons 2-11: $100,000 each

All spending comes from these stocks of wealth.

Now assume a very simple consumption function — a two-step “curve” — based on MPC (and marginal utility of consumption) thinking: propensity to consume for those holding more than $500,000 is 3% (because that satisfies their desires), while it’s 5% for those holding less than $500K.

Here’s how spending (Y, or GDP) plays out:

.05 x $100K x 10 = $50,000

+ .03 x $1 mil = $30,000

= $80,000

Now change the initial wealth setting: Persons 2-11 have $50,000 each, and Person 1 has $1.5 million.

.05 x $50K x 10 = $25,000

+ .03 x $1.5 mil = $45,000

= $70,000

By transferring half of the poorer people’s money to the richer person, we’ve cut GDP by $10,000, or 12.5%.

Then consider the change in shares of wealth from 2007-2010. Median net worth dropped by 40%, while the net worth of the top 10% went up.

Even if you accept the notion that predicted income constitutes a large portion of people’s perceived “wealth,” the implications are the same. If more of the national income (the $80K or $70K in spending) goes to the poorer people, they will have more wealth in future periods, with the salutary effects on GDP and prosperity shown above. (If they expect that distribution to continue, it will even impact their estimates of their own wealth in this period, increasing their current propensity to spend/consume.)

And this doesn’t even consider declining marginal utility of consumption (or only includes it in a display of circular logic) — that somebody with a $25,000 consumption budget gets more utility from a given (percentage or absolute) budget increase than one with a $50,000 consumption budget. So a small percentage shift in shares of wealth from the rich to the poor, or vice versa, results in quite large shifts in shares of our aggregate utility.

A supporting argument from the personal-anecdote-as-the-singular-of-“data” school of rhetoric: all this holds true for me. I put away a very nice chunk some years back, and am playing the fairly typical “will I run out first or die first?” game. (It’s hard to say which is worse. How many people spend their last dollar on the day they die?) I’ve often joked with my financial advisor that I have one Key Economic Indicator: how much money do I have? That’s what I think about when deciding whether to spend. People nearing or in retirement start paying a lot more attention to wealth than income. (Related but tangential: not surprisingly, as the future gets closer and more predictable, as the kids get up on their own feet, for instance, “the marginal propensity to consume (MPC) out of wealth increases with the age of the consumer.” PDF.) And we have an increasing number of people in or near retirement these days.

If this thinking holds any water — that the distribution/concentration of (perceived) wealth has an important impact on aggregate marginal propensity to consume — there’s a very solid and rather straightforward theoretical basis for the otherwise largely limp-wristed assertions that we’re starting to hear more glimmers of these days in the mainstream media, and in the more influential sectors of the econoblogosphere.

Equity and economic efficiency are not in conflict. Quite the contrary, in fact.

For those who prefer to look at pesky things like facts, the empirical data bears this out: at least in prosperous countries, greater wealth equality correlates with greater long-term prosperity.

For those who care to hear a personal account of how modest, widespread wealth dispersal can encourage innovation, entrepreneurship, and wealth-creation, see here.

Cross-posted at Angry Bear.

Comments

7 responses to “GDP, Prosperity, The Wealth Effect, and Marginal Propensity to Consume”

It’s funny–I keep reading that as “…don’t you know, we *have* our rents.”

When the excessive inequality comes from parasitic extraction of rents from productivity, it can’t do anything but harm “long-term prosperity.” Rentiers *don’t* plow money back into investment in corporate infrastructure and growth–let alone employee wages or benefits. It’s a kind of economic sabotage–but these guys are the ones we’re supposed to salute as “job creators.” For them, it’s a zero-sum game, and they’re “winning.”

Thanks,

Ole

I’m with you on this, but I do hesitate to fully adopt the more radical dismissals of “rent” as being morally valid or socially useful. If I build a house and rent it to you, is that income morally suspect? Is it more so if I pay somebody else to build the house? In either case, does the whole process/ecosystem benefit society (and which parts of society)? I think this needs to be carefully theorized — something I’m not going to do here…

[…] that says consumption by the super rich can continue to drive the economy. But I like how Roth dissects that argument using Marginal Propensity to Consume. Basically poor people spend a greater […]

[…] that says consumption by the super rich can continue to drive the economy. But I like how Roth dissects that argument using Marginal Propensity to Consume. Basically poor people spend a greater […]

[…] declining marginal propensity to spend out of wealth. (Something I fiddled with previously, here.) That in turn is based on the declining marginal utility of consumption (the millionth dollar […]

[…] illustrated to me by Ananya Roy‘s talk at TEDx Berkeley this year. I also get that having a middle class is probably important since the uber rich simply won’t purchase enough super-yachts to keep the economy chugging […]

[…] illustrated to me by Ananya Roy‘s talk at TEDx Berkeley this year. I also get that having a middle class is probably important since the uber rich simply won’t purchase enough super-yachts to keep the economy chugging […]